Understanding Inventory Management

Inventory management is a critical aspect of supply chain and business operations that involves overseeing and controlling the flow of goods, raw materials, and finished products within a company. It plays a pivotal role in ensuring that a business has the right amount of inventory at the right time, minimizing costs, and optimizing overall efficiency.

Importance of Inventory Management

Effective inventory management is crucial for several reasons. Firstly, it helps businesses avoid stockouts and overstock situations, both of which can be detrimental to a company’s bottom line. Stockouts can lead to lost sales, customer dissatisfaction, and damage to a company’s reputation. On the other hand, overstocking ties up capital incurs holding costs, and may result in product obsolescence.

Secondly, inventory management contributes to improved cash flow. By maintaining optimal inventory levels, a company can free up capital that would otherwise be tied up in excess stock. This capital can then be invested in other areas of the business, promoting growth and financial stability.

Thirdly, effective inventory management enhances operational efficiency. It ensures that goods are available when needed, minimizing production delays and ensuring timely order fulfillment. This, in turn, helps in building customer trust and loyalty.

Key Components of Inventory Management

Inventory management encompasses various key components that work together to maintain an efficient and balanced supply chain. These components include demand forecasting, order placement, stock tracking, and replenishment strategies.

Demand forecasting involves predicting the demand for products based on historical data, market trends, and other relevant factors. Accurate forecasting enables companies to plan their production and procurement activities, preventing both excess and insufficient inventory levels.

Order placement is the process of determining when and how much to order. This involves setting reorder points and order quantities, taking into account lead times, demand variability, and other factors. A well-defined order placement strategy ensures that a company maintains optimal inventory levels without incurring unnecessary costs.

Stock tracking is the ongoing monitoring of inventory levels. This involves the use of technology, such as barcoding or RFID systems, to keep real-time records of stock movements. Accurate stock tracking allows businesses to identify discrepancies, prevent theft or loss, and make informed decisions regarding reordering.

Replenishment strategies involve determining how and when to replenish inventory. This includes decisions about restocking intervals, safety stock levels, and the use of economic order quantity (EOQ) models. An effective replenishment strategy ensures that inventory is replenished in a timely manner, preventing stockouts and minimizing holding costs.

Understanding inventory management involves recognizing its importance in achieving operational excellence and the key components that contribute to its success. A well-managed inventory not only ensures a smooth supply chain but also positively impacts a company’s financial health and customer satisfaction.

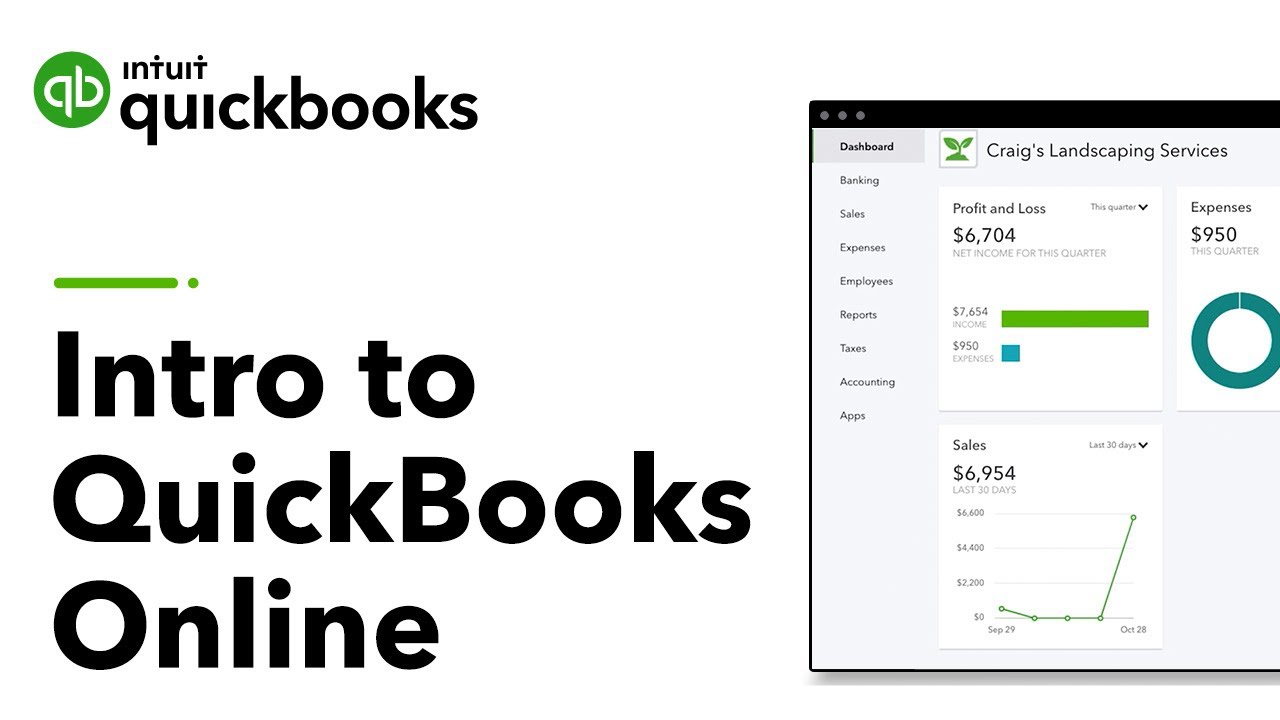

Introduction to QuickBooks

QuickBooks is a comprehensive accounting software designed to streamline financial management for businesses of all sizes. It provides a user-friendly platform that allows users to efficiently manage their finances, track expenses, and generate various financial reports. One of the key features that sets QuickBooks apart is its capability to handle inventory management seamlessly, making it a valuable tool for businesses involved in buying and selling products.

Overview of QuickBooks

In essence, QuickBooks serves as a centralized hub for all financial transactions within a business. It enables users to create and send invoices, track sales and expenses, reconcile bank statements, and manage payroll. The software’s intuitive interface and customizable features cater to the diverse needs of different industries. QuickBooks helps businesses maintain accurate and up-to-date financial records, facilitating better decision-making and financial analysis.

Versions with Inventory Features

QuickBooks offers various versions to cater to different business requirements, and specific versions come with enhanced inventory management features. For example, QuickBooks Desktop Premier and QuickBooks Desktop Enterprise are versions that include advanced inventory tools. These tools allow businesses to track inventory levels, set reorder points, and manage stock efficiently. This is particularly beneficial for retail, manufacturing, and distribution businesses that rely heavily on inventory control for smooth operations.

Setting up QuickBooks for Inventory Management

Setting up QuickBooks for inventory management is a crucial step to ensure accurate tracking and efficient control of stock. The process involves entering product details, including item names, descriptions, and quantities. Users can also set up categories and subcategories to organize products systematically. Additionally, it’s essential to input the cost and selling price of each item to facilitate accurate financial reporting.

Furthermore, users can utilize QuickBooks features such as barcode scanning, which helps in the quick and error-free entry of inventory data. Integration with other business applications, such as point-of-sale systems or e-commerce platforms, can further streamline the inventory management process. Proper setup ensures that QuickBooks becomes a powerful tool for maintaining optimal stock levels, reducing the risk of overstock or stockouts, and improving overall business efficiency.

QuickBooks stands as a versatile accounting solution with robust inventory management capabilities. Understanding its overview, available versions with inventory features, and the process of setting it up for inventory management is pivotal for businesses seeking to leverage the full potential of this software in their day-to-day operations.

QuickBooks Inventory Features

QuickBooks, a popular accounting software, offers a robust set of inventory management features that cater to the needs of businesses across various industries. These features play a crucial role in helping businesses streamline their operations and maintain accurate records of their inventory. In this discussion, we’ll delve into each of the QuickBooks inventory features in more detail.

Inventory Tracking:

One of QuickBooks’ fundamental inventory features is inventory tracking. This feature enables businesses to monitor their stock levels in real-time. It allows users to keep track of the quantity of each item they have on hand, providing visibility into product availability. With accurate inventory tracking, businesses can avoid stockouts, fulfill customer orders efficiently, and make informed decisions about restocking.

Inventory Valuation:

QuickBooks provides a robust inventory valuation system that helps businesses determine the financial worth of their inventory. By assigning values to individual items based on cost methods such as FIFO (First In, First Out) or average cost, businesses can gain insights into the overall value of their stock. Accurate inventory valuation is crucial for financial reporting, tax compliance, and assessing the profitability of the business.

Adjusting Inventory Levels:

In the dynamic business environment, inventory levels can fluctuate due to various factors such as sales, returns, or damaged goods. QuickBooks allows users to easily adjust inventory levels to reflect these changes accurately. This feature ensures that the system stays aligned with the actual physical inventory on hand, preventing discrepancies between recorded and actual stock levels.

Backordering:

QuickBooks facilitates efficient order management through its backordering feature. When items are out of stock, businesses can still accept customer orders and create backorders. This allows for a seamless order fulfillment process once the items become available again. Backordering helps maintain customer satisfaction by preventing the loss of sales opportunities and keeping customers informed about the status of their orders.

Customizing Inventory Reports:

To meet the diverse reporting needs of businesses, QuickBooks offers the flexibility to customize inventory reports. Users can tailor reports to display specific information such as stock levels, sales trends, or inventory valuation. Customizable reports empower businesses to analyze data in a way that aligns with their unique requirements, facilitating better decision-making and strategic planning.

QuickBooks’ inventory features provide businesses with powerful tools to manage their stock effectively, optimize operations, and enhance overall efficiency in the realm of inventory management. Whether it’s tracking stock levels, valuing inventory accurately, adjusting levels as needed, managing backorders, or generating customized reports, QuickBooks equips businesses with a comprehensive suite of features to navigate the complexities of inventory management.

Setting up Inventory in QuickBooks

Setting up inventory in QuickBooks is a crucial step for businesses that need to manage and track their products or services. This process involves several key components to ensure accurate and efficient inventory management. In this description, we’ll delve into each step in more detail.

Adding Products and Services:

The first step in setting up inventory in QuickBooks is adding products and services to your account. This involves inputting detailed information about each item you sell or stock. This information may include the product or service name, description, sales price, cost, and any other relevant details. By adding this information, you create a comprehensive database of your inventory that QuickBooks can use for various purposes, such as generating sales reports and tracking stock levels.

Categorizing Items:

Once you’ve added your products and services, it’s important to categorize them appropriately. Categorization helps organize your inventory and makes it easier to analyze sales trends and financial data. QuickBooks allows you to create custom categories or use predefined ones to group similar items together. This categorization not only streamlines your reporting but also enhances your ability to make informed business decisions based on product categories.

Setting Up Units of Measure:

For businesses dealing with diverse products that come in varying units of measure, setting up units of measure in QuickBooks is essential. This feature allows you to specify how each product is measured or counted. Whether it’s by quantity, weight, volume, or any other unit, QuickBooks accommodates your specific needs. This functionality is particularly useful for businesses with complex inventory management requirements, ensuring accuracy in tracking and reporting.

Enabling Inventory Tracking for Items:

The final step is to enable inventory tracking for items in QuickBooks. This feature allows you to monitor the quantity of each product or service in stock, track sales, and generate real-time reports on inventory levels. By activating inventory tracking, you gain visibility into stock movements, helping prevent stockouts or overstock situations. This is critical for businesses looking to optimize their inventory management processes and maintain a healthy balance between supply and demand.

Setting up inventory in QuickBooks involves a systematic approach that includes adding detailed information, categorizing items, setting up units of measure, and enabling inventory tracking. This comprehensive setup not only ensures accurate record-keeping but also equips businesses with the tools needed to make informed decisions regarding their inventory and overall financial health.

Managing Stock Levels

Effective stock management is crucial for the smooth operation of any business. It involves various processes and tools to ensure that the right products are available at the right time. This entails tracking stock quantity, setting reorder points, managing overstock and understock situations, and utilizing QuickBooks notifications to streamline the entire process.

Tracking Stock Quantity

The first step in managing stock levels is accurately tracking the quantity of each product in inventory. This involves implementing systems, such as barcoding or inventory management software, to keep a real-time record of stock levels. Regular audits and reconciliations are also essential to identify any discrepancies between recorded and actual stock quantities. Tracking stock quantity helps businesses maintain optimal inventory levels and avoid shortages or excess stock.

Setting Reorder Points

To prevent stockouts and maintain a continuous supply chain, businesses establish reorder points for their products. Reorder points are predetermined stock levels that trigger the replenishment process. This proactive approach ensures that orders are placed in a timely manner, minimizing the risk of running out of popular products. The reorder point is often determined by considering factors like lead time, sales velocity, and desired safety stock levels.

Managing Overstock and Understock

Balancing stock levels is a delicate act that requires careful attention to both overstock and understock situations. Overstock can lead to storage issues, increased holding costs, and potential obsolescence, while understock may result in lost sales, dissatisfied customers, and disruptions in the supply chain. Regular analysis of sales trends, demand forecasting, and adjusting reorder points help in avoiding these pitfalls, ensuring that stock levels align with market demand.

Utilizing QuickBooks Notifications

QuickBooks, a popular accounting software, offers features that can significantly aid in managing stock levels. One such feature is the ability to set up notifications. QuickBooks notifications can be configured to alert businesses when stock levels reach predefined thresholds, helping them stay informed in real-time. This timely information enables quick decision-making, allowing businesses to reorder products, adjust pricing, or implement marketing strategies based on the current stock situation.

Managing stock levels is a multifaceted process that involves tracking stock quantity, setting reorder points, and effectively managing both overstock and understock situations. Leveraging tools like QuickBooks with its notification features enhances the efficiency of these processes, contributing to a well-organized and responsive inventory management system.

Using QuickBooks for Purchase Orders

QuickBooks is a comprehensive accounting software that offers robust features for managing various aspects of business finances. One key functionality is its ability to streamline the Purchase Order (PO) process, providing businesses with an efficient means of tracking and managing their procurement activities.

Creating Purchase Orders:

The creation of Purchase Orders is a fundamental aspect of the procurement process. QuickBooks simplifies this task by offering a user-friendly interface that allows users to input relevant details such as item descriptions, quantities, prices, and vendor information. Users can easily customize templates, ensuring that each PO aligns with the specific needs of the business. This feature not only saves time but also reduces the likelihood of errors in the procurement documentation.

Moreover, QuickBooks allows for seamless integration with other modules, such as inventory management and expense tracking. This integration ensures that the creation of purchase orders is a cohesive part of the overall financial management process. It also enables businesses to maintain accurate records and provides real-time visibility into their purchasing activities.

Tracking PO Status:

Efficient tracking of Purchase Order status is crucial for businesses to maintain control over their procurement processes. QuickBooks facilitates this by offering a centralized platform where users can monitor the status of each PO in real-time. The software provides updates on order approvals, shipments, and delivery dates, enabling businesses to proactively manage their inventory and respond promptly to any changes in the procurement pipeline.

The tracking feature in QuickBooks not only enhances transparency but also aids in identifying potential bottlenecks or delays in the procurement cycle. This proactive approach enables businesses to take corrective actions promptly, ensuring that they can meet their operational needs and maintain positive relationships with vendors.

Vendor Management:

QuickBooks extends its utility beyond the creation and tracking of purchase orders to encompass effective vendor management. Businesses can leverage the platform to maintain a comprehensive vendor database, including contact information, payment terms, and performance history. This centralized vendor management system enhances efficiency by eliminating the need for manual record-keeping and reducing the likelihood of errors.

Furthermore, QuickBooks facilitates seamless communication with vendors by allowing users to send POs directly through the system. This not only expedites the procurement process but also ensures that both parties have a consistent record of transactions. Additionally, the software provides insights into vendor performance, helping businesses make informed decisions about their supplier relationships.

QuickBooks offers a robust suite of tools for managing the end-to-end purchase order process. From creating customized POs to real-time tracking and efficient vendor management, businesses can leverage these features to streamline their procurement activities and enhance overall financial control.

Sales Orders and Invoicing

Sales Orders and Invoicing are critical components of the sales process in any business. These activities involve creating sales orders, generating invoices, and managing sales receipts to ensure a smooth and transparent financial transaction process. Let’s delve deeper into each aspect:

Creating Sales Orders

Sales orders are pivotal documents that initiate the sales process. They serve as a formal request made by a customer to purchase goods or services from a business. When creating sales orders, businesses capture essential details such as the customer’s information, the items or services requested, quantities, and agreed-upon prices. This document not only acts as a confirmation of the customer’s intent to buy but also serves as a reference for inventory management and order fulfillment.

Invoicing and Sales Receipts

Invoicing is the next crucial step in the sales cycle. Once the products or services have been delivered or provided, businesses generate invoices to request payment from the customer. Invoices typically include details such as the billing information, a breakdown of the products or services provided, their respective prices, and the total amount due. The timely and accurate creation of invoices is vital for maintaining healthy cash flow and establishing a transparent financial relationship with customers.

Sales receipts play a complementary role in the process, serving as a confirmation of payment received. When a customer remits payment for the products or services, a sales receipt is issued to acknowledge and document the transaction. This receipt can be crucial for both parties as proof of the completed payment, and it contributes to the overall record-keeping and financial reconciliation processes within the business.

Fulfilling Orders from Inventory

Fulfilling orders from inventory is the operational aspect of the sales process. Once a sales order is received and confirmed, businesses need to fulfill the order by picking the requested items from their inventory and preparing them for shipment or delivery. Efficient inventory management is crucial in this phase to ensure that products are available, accurate quantities are selected, and any potential issues with stock shortages or discrepancies are addressed promptly. Successful order fulfillment contributes to customer satisfaction and helps in maintaining a positive reputation for the business.

The seamless coordination of creating sales orders, generating invoices, and fulfilling orders from inventory is essential for the success of any business. These processes not only facilitate financial transactions but also play a pivotal role in customer satisfaction, inventory management, and overall business operations. Businesses that effectively manage these aspects contribute to a smoother sales cycle and build a foundation for long-term success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}