QuickBooks Chart of Accounts Setup

The Chart of Accounts is a foundational element in the field of accounting, serving as a comprehensive and organized list of all the accounts employed by a business to document its financial transactions. This essential tool provides a systematic structure that aids in the classification and arrangement of financial data, forming the backbone of an organization’s accounting system.

One of the key functions of the Chart of Accounts is to enhance the accuracy of financial record-keeping. By categorizing accounts in a logical and standardized manner, the chart enables consistent and precise recording of various financial activities. This systematic approach not only simplifies the data entry process but also reduces the likelihood of errors, ensuring the integrity and reliability of the financial information.

Components and Structure:

The Chart of Accounts comprises various components, each serving a distinct role in the organization’s financial framework. Typically organized in a hierarchical structure, it includes main categories, subcategories, and individual accounts. Main categories often represent broad classifications such as assets, liabilities, equity, revenue, and expenses. Subcategories and individual accounts further break down these main categories into more specific items.

For example, under the main category of expenses, subcategories could include operating expenses, administrative expenses, and selling expenses. Individual accounts within these subcategories might then specify particular expenses like utilities, rent, or advertising costs. This hierarchical arrangement allows for a detailed and granular view of a company’s financial transactions, offering insights into specific areas of financial performance.

Flexibility and Adaptability:

A notable characteristic of the Chart of Accounts is its flexibility and adaptability. Businesses can tailor their charts to align with their specific needs, industry requirements, and reporting preferences. This flexibility enables organizations to modify their charts as their operations evolve, ensuring that the accounting system remains relevant and reflective of the business’s financial structure.

Moreover, the Chart of Accounts is not static; it can be adjusted to accommodate changes in accounting standards, regulatory requirements, or shifts in business strategy. This adaptability is crucial for maintaining compliance, accurately reflecting financial positions, and supporting strategic decision-making within the dynamic business environment.

The Chart of Accounts is a dynamic and essential tool that plays a pivotal role in organizing, categorizing, and recording financial transactions for businesses. Its structured framework enhances accuracy, provides a detailed view of financial activities, and allows for flexibility to meet the evolving needs of the organization and external reporting standards.

Types of QuickBooks Chart of Accounts Setup:

In accounting, various types of accounts are used to categorize and organize financial transactions. These accounts fall into five main categories: Asset Accounts, Liability Accounts, Equity Accounts, Income Accounts, and Expense Accounts.

Asset Accounts:

Asset accounts represent the economic resources owned by a business. These are divided into three subcategories:

Current Assets: These are short-term assets that are expected to be converted into cash or used up within a year. Examples include cash, accounts receivable, and inventory.

Fixed Assets: Also known as long-term assets, these are tangible or intangible assets that have a useful life beyond one year. Examples include buildings, machinery, and patents.

Other Assets: This category includes any other assets that don’t fit into the above subcategories, such as prepaid expenses.

Liability Accounts:

Liability accounts represent the obligations or debts of a business. There are two main subcategories:

Current Liabilities: These are short-term obligations that are due within a year, such as accounts payable and short-term loans.

Long-Term Liabilities: These are obligations with a maturity date beyond one year, like long-term loans and bonds payable.

Equity Accounts:

Equity accounts represent the owner’s interest in the business and the retained earnings. There are two primary subcategories:

Owner’s Equity: This represents the owner’s investment in the business and is calculated as assets minus liabilities. It’s essentially the owner’s claim on the company’s assets.

Retained Earnings: This account tracks the cumulative profits or losses that the company has retained over time. It is a component of owner’s equity.

Income Accounts:

Income accounts track the revenues generated by the business. The main subcategories include:

Sales: This represents the total revenue generated from selling goods or services.

Service Income: This includes revenue generated from providing services rather than selling physical goods.

Other Income: Any additional income that doesn’t fall into the above categories, such as interest income.

Expense Accounts:

Expense accounts represent the costs incurred by a business to generate revenue. These are divided into three subcategories:

Cost of Goods Sold (COGS): This includes the direct costs associated with producing goods or services sold by the company.

Operating Expenses: These are general and administrative costs necessary for running the business, such as rent, utilities, and salaries.

Other Expenses: This category encompasses any other expenses not covered by COGS or operating expenses, like interest and taxes.

Importance of a QuickBooks Chart of Accounts Setup:

Accurate Financial Reporting:

A well-organized Chart of Accounts serves as the backbone for accurate financial reporting within a business. By categorizing various financial elements such as income, expenses, assets, and liabilities, it provides a systematic structure for tracking and recording financial transactions. This organized framework ensures that the financial reports generated are precise and reliable. Management and stakeholders heavily rely on these reports for decision-making, making the accuracy of financial information paramount.

Streamlined Bookkeeping:

The efficiency of bookkeeping processes is significantly enhanced by a well-structured Chart of Accounts. This organizational tool serves as a roadmap for data entry, offering a clear and systematic approach to recording financial transactions. With properly defined accounts, bookkeepers can easily identify where each transaction belongs, reducing the likelihood of errors in recording. This streamlined bookkeeping process not only saves time but also enhances the overall accuracy and reliability of the financial data.

Tax Compliance:

Maintaining a properly organized Chart of Accounts is crucial for ensuring tax compliance. The categorization of accounts facilitates the seamless generation of reports that adhere to tax regulations. In particular, software like QuickBooks leverages the Chart of Accounts to produce reports that are specifically tailored for tax purposes. This not only simplifies the tax reporting process but also minimizes the risk of errors and discrepancies, ultimately contributing to a smoother and more compliant tax filing experience for businesses. By having a well-maintained Chart of Accounts, businesses can navigate the complexities of tax regulations more effectively.

Customizing the Chart of Accounts:

One fundamental aspect of efficient financial management is customizing the Chart of Accounts. This organizational tool serves as the backbone of a company’s accounting system. Customization allows businesses to tailor their Chart of Accounts to precisely fit their unique financial structure and reporting needs.

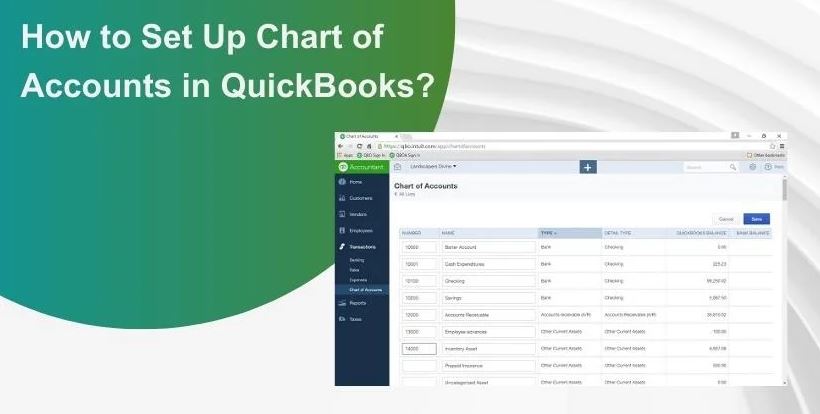

Accessing the Chart of Accounts:

To begin the customization process, access the Chart of Accounts through your accounting software. Navigate to the “Lists” menu, and within it, select the “Chart of Accounts.” This centralized location is where you can view, modify, and add accounts based on your business requirements.

Editing or Adding Accounts:

Once in the Chart of Accounts, you have the flexibility to edit existing accounts or add new ones. Editing involves modifying account details to better align with your evolving business dynamics. To add a new account, choose the “Account” option and then select “New.” This straightforward process allows for the seamless integration of accounts tailored to your specific financial activities.

Account Types and Detail Types:

When customizing accounts, it’s crucial to understand the different account types available, such as Asset, Liability, Equity, Income, and Expense. Select the appropriate type based on the nature of the financial activity. Further refinement is achieved by specifying the detail type, which provides a more granular categorization of the account. This level of specificity enhances accuracy in financial reporting and analysis.

Account Naming Conventions:

Effective communication in accounting relies heavily on clear and concise naming conventions for each account. The importance of avoiding confusion cannot be overstated. Develop a naming convention that is not only reflective of your business but also aligns with industry standards. This consistency aids in streamlining financial processes and ensures that financial statements are easily understandable to stakeholders.

Follow a naming convention that aligns with your industry and business structure:

Consistency in naming conventions is paramount. Ensure that your chosen convention aligns with industry standards and your specific business structure. This alignment fosters a standardized approach across your financial reporting, making it comprehensible to internal and external parties. Striking this balance between customization and industry norms is key to a robust and adaptable Chart of Accounts.

Setting Up the Chart of Accounts in QuickBooks:

Setting up the chart of accounts in QuickBooks is a crucial step in establishing the financial framework for your business. This process involves several steps, and one of the initial stages is creating a new company file.

To initiate the creation of a new company file, the first step is to launch QuickBooks on your computer. Once the software is open, you’ll be presented with options such as “Create a new company” or “Start Setup.” Choosing either of these options will kickstart the setup process.

As you proceed, QuickBooks will guide you through a series of on-screen prompts designed to gather essential information about your company. This includes entering details such as your company’s name, address, contact information, and other relevant identifiers. Providing accurate and comprehensive information at this stage ensures that your company file is properly configured to suit your specific business needs.

In addition to basic company details, you will be prompted to specify your industry type. QuickBooks tailor certain settings and features based on the industry to better align with the unique financial requirements of different businesses. Selecting the correct industry type helps in customizing your chart of accounts and other financial settings appropriately.

Furthermore, during the setup process, you will be required to define your fiscal year. This is a critical aspect as it establishes the starting and ending dates for your financial reporting period. Setting the fiscal year accurately is vital for maintaining consistency in financial reporting and aligning with regulatory requirements.

Creating a new company file in QuickBooks involves launching the software, entering comprehensive company information, specifying industry type, and setting up the fiscal year. These initial steps lay the foundation for the subsequent configuration of the chart of accounts and other financial settings, ensuring that QuickBooks is tailored to your business’s unique financial structure.

Advanced QuickBooks Chart of Accounts Setup:

Sub-Accounts and Parent Accounts:

Creating Sub-Accounts:

In the realm of accounting, the ability to enhance granularity is paramount. The introduction of sub-accounts under main accounts offers a powerful tool for achieving this. This customization feature allows for a more detailed tracking system within broader categories. Businesses can meticulously organize and analyze financial transactions, gaining insights into specific aspects of their operations.

Linking Sub-Accounts to Parent Accounts:

The establishment of relationships between sub-accounts and their parent accounts brings a hierarchical structure to the financial data. This linkage enables a comprehensive and organized view of the company’s financial landscape. Users can navigate through the levels of accounts, understanding the connections and dependencies, ultimately facilitating more informed decision-making.

Account Numbers:

Enabling Account Numbers:

QuickBooks provides users with the flexibility to assign account numbers to various accounts within the chart of accounts. This functionality streamlines the identification process, offering a quick and efficient means of locating specific accounts. By enabling account numbers, businesses can significantly reduce the time and effort required for financial analysis and reporting.

Numbering System:

The effectiveness of utilizing account numbers is further enhanced by choosing a numbering system that aligns with the business structure. This step ensures consistency and coherence in the numbering scheme, avoiding confusion and errors in financial documentation. A well-thought-out numbering system contributes to the overall clarity and ease of use, promoting a more efficient and accurate accounting process.

The advanced chart of accounts customization features, including sub-accounts with parent relationships and the use of account numbers, empowers businesses to tailor their financial tracking systems to suit their specific needs. These tools not only enhance the granularity of financial data but also streamline the identification and organization of accounts, ultimately contributing to more informed decision-making and efficient accounting processes.

Best Practices for Chart of Accounts Management:

Regular Review and Updates:

- Periodic Evaluation:

Maintaining a dynamic and accurate Chart of Accounts is crucial for reflecting the evolving nature of a business. Regular reviews should be conducted to assess the relevance of existing accounts. Changes in business operations, expansions, or contractions may necessitate adjustments to the account structure. By periodically evaluating the Chart of Accounts, discrepancies and inefficiencies can be identified and promptly addressed.

- Update Accounts Based on Changes:

Business environments are subject to constant change, be it in products, services, or organizational structure. It is essential to update the Chart of Accounts in response to these changes. This ensures that financial reporting remains accurate and aligned with the current state of the business. An agile and responsive approach to updates helps prevent the accumulation of outdated or irrelevant account entries.

Collaboration and Consultation:

- Involving Stakeholders:

Effective Chart of Accounts management goes beyond the accounting department. Collaborating with key stakeholders from different departments is crucial for capturing diverse perspectives on account structure. Involving department heads and managers in the decision-making process ensures that the Chart of Accounts aligns with the specific needs and reporting requirements of each business unit. This collaborative approach fosters a sense of ownership and accountability among stakeholders.

- Professional Advice:

Navigating the complexities of account categorization may require specialized knowledge. Seeking guidance from accounting professionals provides valuable insights and ensures that the Chart of Accounts adheres to industry standards and best practices. Professional advice becomes particularly important when encountering ambiguous or unique transactions that may pose challenges in categorization. Leveraging the expertise of accounting professionals contributes to the optimal setup and functionality of the Chart of Accounts.

- Leverage Industry-Specific Knowledge:

Every industry has its nuances and specific requirements when it comes to financial reporting. The chart of Accounts setup should take into account these industry-specific considerations. By leveraging industry-specific knowledge, businesses can tailor their account structure to meet regulatory compliance and reporting standards relevant to their sector. This approach not only enhances accuracy but also streamlines financial processes by aligning them with industry norms.

The effective management of a Chart of Accounts involves a combination of regular reviews, collaborative decision-making with stakeholders, and seeking professional advice when needed. By following these best practices, businesses can ensure that their Chart of Accounts remains a dynamic and reliable tool for financial management and reporting.

Troubleshooting and Common Mistakes:

In the realm of financial management, troubleshooting plays a pivotal role in maintaining accuracy and reliability. Errors can emerge from various sources, including data entry mishaps, software glitches, or procedural misunderstandings. Identifying and rectifying these issues is essential for the overall integrity of financial records.

Error Identification and Correction:

One crucial aspect of troubleshooting involves the diligent identification and correction of errors. This process starts with the regular generation of financial reports. These reports serve as a snapshot of the organization’s financial health, revealing discrepancies that might otherwise go unnoticed. Timely and systematic reviews of these reports are imperative for spotting anomalies.

Reviewing Reports:

Financial reports encapsulate a comprehensive overview of an organization’s monetary transactions. Regularly reviewing these reports helps in staying vigilant against potential inaccuracies. This practice not only ensures financial transparency but also aids in decision-making processes. Thorough scrutiny of line items, balances, and trends provides insights into the financial health of the organization.

Investigate and Correct:

Upon identifying discrepancies in financial reports, the next step is a thorough investigation. This involves delving into the details of transactions, cross-referencing data, and understanding the context of the errors. Swift and precise corrective actions should follow the investigation. This might involve adjusting entries, rectifying data entries, or addressing any systemic issues contributing to the errors.

Prompt Action:

The importance of prompt action cannot be overstated in the context of error correction. Delayed responses can lead to compounding issues and make it challenging to trace the origins of errors. Timeliness is of the essence in maintaining financial accuracy and upholding the trust of stakeholders.

Conclusion:

In conclusion, the QuickBooks Chart of Accounts Setup is a fundamental component of effective financial management in QuickBooks. By understanding its significance, structuring it appropriately, and implementing best practices, businesses can leverage this tool to streamline their accounting processes, enhance reporting accuracy, and ensure compliance with tax regulations. Taking the time to set up and maintain a well-organized Chart of Accounts is an investment that pays dividends in the form of improved financial visibility and decision-making capabilities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}